Hey, all! I hope you had a great weekend. Today, we dive into what’s driving markets and what the near future may look like. On Monday, we will do deeper dives like this. Friday, we’ll try for recaps. Trade ideas are coming soon via monthly research, which will look similar to this linked document.

Market momentum slowed with bumps in economic and inflation data last week, yet the trend of economic resilience and declining inflation persists. Anticipation looms over a potential shift in the Federal Reserve’s approach, with traders awaiting Tuesday for insights from Governor Christopher Waller regarding the possibility of a decrease in interest rates.

CrossBorder Capital remarks the economy may avoid recession, attributing this to economic measures adjusted for distortion—an increase in adjusted yields points to a mild recovery in business activity later in the year.

Former open markets trader Joseph Wang maintains cautious optimism, foreseeing cuts, albeit less aggressive than the market prices. However, Cem Karsan from Kai Volatility suggests that if anticipated stock struggles and declines reach 10% or more, more decisive, politically motivated actions may be taken ahead of the election.

In any case, injecting money into a healthy economy is bullish. That being so, Goldman Sachs foresees the S&P 500 reaching 4,950 to 5,050 by 2025. Wang, emphasizing the potential benefits of both monetary and fiscal stimulus, notes deficit spending ultimately triggers an increase in both yields and risk assets like stocks.

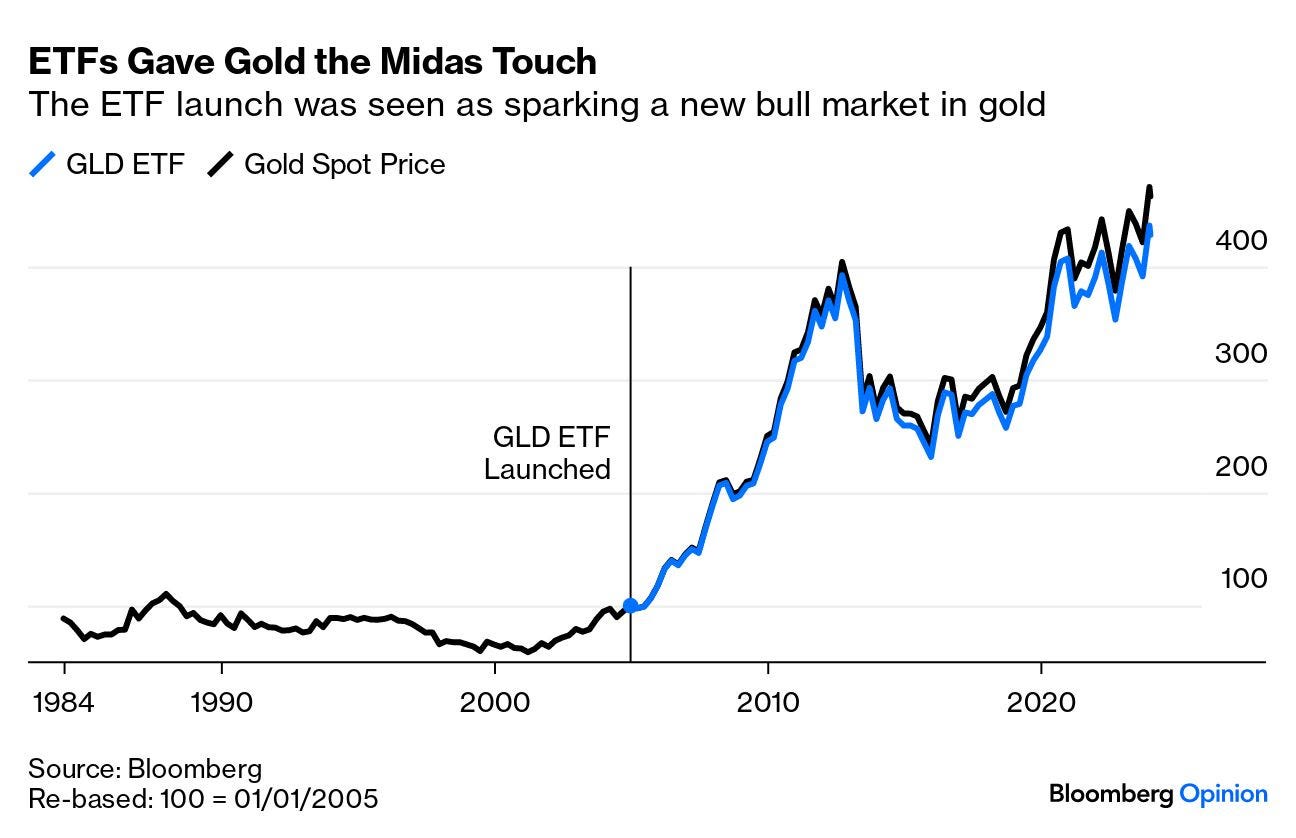

Cryptocurrencies may also benefit, with some anticipating the approval of a bitcoin exchange-traded fund to invigorate a bullish trend akin to the impact of State Street's Gold Trust on the gold market. However, not all share this optimism, including Tom McClellan, who parallels a situation in 1974 when investors bid up gold prices in anticipation of Americans regaining the right to own gold, only to witness a decline of 41% in prices by August 1976.

Whether higher rates persist or not, specific forces are at play that are unlikely to destabilize the market markedly. Elevated rates give rise to an increased demand for what is termed “one-sided and risky positioning,” elongating the market cycle and reducing short-term volatility through mechanical interventions. This artificial stability sends misleading signals, fostering even more interest in this type of trading. Karsan aptly dubs it the “sumomarket,” echoing Amy Wu Silverman of RBC Capital Markets' insight that such strategies aren’t indefinite and may sour.

We hedge when we can, not when we must! Traditional reliance on bonds falls short in a landscape where correlations have transformed. During the subdued realized and implied volatility, traders protect against pullbacks, particularly during or after the earnings season, by buying Cboe VIX call options.

In the realm of alternatives, the choice depends on your timeframe and view on price trajectories. We gave explanations last year, revealing options like allocating principal to less risky assets such as box spreads utilized as collateral for margin-intensive trades. For those eyeing the short-term downside, ultra-wide butterflies—equidistant or slightly broken—emerge as a consideration. Contrastingly, if it were 2022, cheaper ratio spreads would be preferred due to the subdued tendencies of implied volatility. However, with “over-positioning into short volatility,” that may no longer be the case.

As per Fedwatching: "FOMC voters have said over and over that 2% is the target. Getting inflation down to 2-ish (say 2.5%) is probably not good enough. If we’re still at 2.5% at the end of the year and the job market is in decent shape, I think it’s more likely that they’ll be hiking instead of cutting." EU and USA are on 2 different paths. Today data of european industrial production, Germania gdp, wholesale price index, italian export are all in "recession mode"