Daily Brief | September 7, 2022 + Case Study

Daily Brief | September 7, 2022 + Case Study

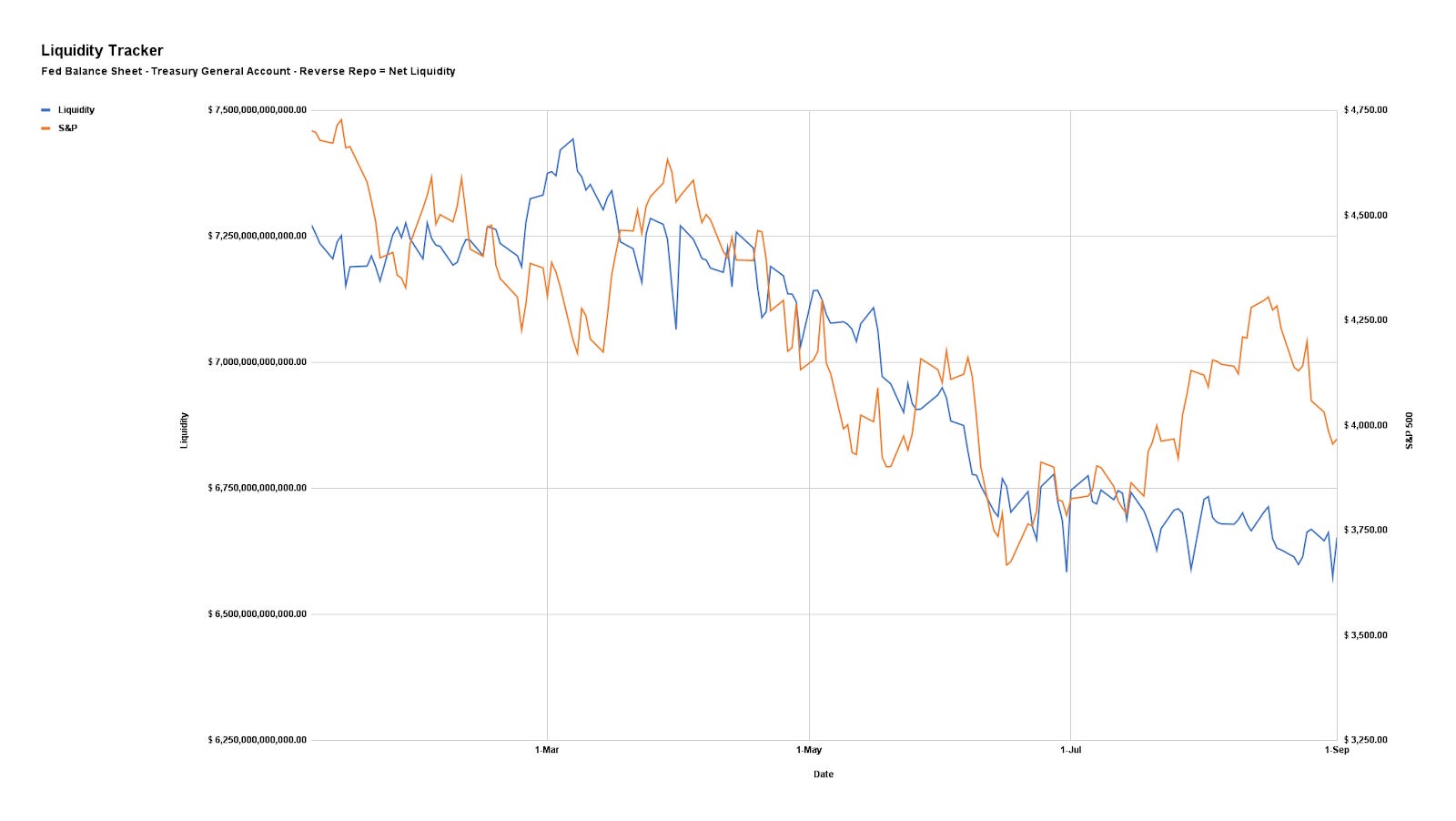

Daily commentary for U.S. broad market indices.

The Daily Brief is a free glimpse into the prevailing fundamental and technical drivers of U.S. equity market products. Join the 850+ that read this report daily, below!

Case Study

Switching it up, today, with a case study! Let me know if this is something you enjoy.

Heading into the 2022 equity market decline, institutions repositioned and hedged their downside, even allocating to commodities, which worked well for the first couple of quarters.

Due in part to this, the 2022 equity market decline was like no other experienced during 2021.

Instead, the monetization and counterparty hedging of existing customer options hedges, as well as the sale of short-dated options, particularly in some of the single names where implied volatility (IVOL) was rich, lent to lackluster performance in IVOL.

Eventually, entities were squeezed out of trades not working.

That means participants rotated out of options and commodities, all the while a macro-type re-leveraging ensued on improvements in inflation data, an earnings season that was better than expected, and “crazy tax receipts,” among other things.

The most recent advance climaxed the week of the August monthly options expiration (OPEX).

Why? Well, heading into that particular week, markets were rising at a fast rate, and call options (i.e., bets on the market upside) were highly demanded.

Those, on the other side of those call option trades (i.e., counterparties), hedged in a manner that was supportive (i.e., counterparties sell calls to customers and buy underlying to hedge exposure).

Eventually, traders’ activity in soon-to-expire options became concentrated at certain strikes – particularly $4,300.00 in the S&P 500 – while IVOL trended lower. The counterparty’s response, then, did more to support prices and reduce movement.

This is because, with the passage of time and declining volatility, options Gamma (i.e., the sensitivity of an option to direction) became more positive and the range of spot prices, across which Delta (i.e., options exposure to direction) shifts rapidly, became a lot smaller.

When options Gamma exposure is more positive, market movements may have a positive impact on the counterparty’s position (i.e., movement is beneficial). If movement is beneficial, and the counterparty is not interested in realizing that benefit, they may hedge in a manner that can stifle market movement.

This is, in part, what happened, in the late stages of the rally. That said, however, soon after the S&P 500 hit $4,300.00, the near-vertical price rise began to sputter and follow-on support, both from a fundamental (e.g., liquidity) and volatility perspective was soon set to worsen.

Why? There was an OPEX that would trigger “a big shift in market positioning,” Nomura Holdings Inc’s (NYSE: NMR) Charlie McElligott explained.

In short, participants’ failure to roll forward their expiring bets on market upside coincided with a message that the Fed would stay tough on inflation. So, it’s the case that after the OPEX, those same bets that were prompting counterparties to stem volatility and bolster equity upside were not rolled forward.

Instead, these bets expired and this is visualized by the drop in Gamma exposures, post-OPEX.

Accordingly, this expiration, combined with technical and fundamental contexts that were prompting funds to “reload[] on short sales,” shocked the market into a higher volatility, negative Gamma environment. In this environment, put options, through which the vast majority of participants speculate on lower prices and protect their downside, solicited far more pressure from counterparties.

Adding, if markets were to continue trading lower, traders were likely to continue rotating into those put options that would bolster this pressure from counterparties.

This happened as shown, below.

This demand for put options protection was reflected by a bid in IVOL. To hedge against this demand for protection and rising IVOL, counterparties sold underlying, compounding bearish fundamental flows.

In late August, data suggested September would have “a very large options position as it is a quarterly OPEX,” SpotGamma said. With that position being “put heavy,” a slide lower, and an increase in IVOL, was likely to drive continued counterparty “shorting” with little “relief until Jackson Hole.”

In expecting markets to trade lower and more volatile, Physik Invest sought to initiate new trades.

At the time, in mid-August, call option premiums were attractive, in part due to interest rates, all the while IVOL metrics seemingly hit a lower bound.

This was observable via a quick check of skew, a plot of the IVOL levels for options across different strike prices. Usually, skew, on the S&P 500, shows a smirk, not a smile.

This meant it was likely that short-dated, wide Put Ratio Spreads had little to lose in a sideways-to-higher market environment. Additionally, call Vertical Spreads above the market were relatively more expensive.

Given the above context, the following analysis unpacks how Physik Invest traded options tied to the S&P 500 leading up to and through the August 19 OPEX, into the Jackson Hole Economic Symposium.

Note: Click here to view all transactions for all accounts involved.

Sequence 1: After a skew smile was observed, through August 12, 2022, the following positions were initiated, while the S&P 500 was still trending higher, for a net $7,616.68 credit.

Positions were structured in a way that would potentially net higher credits had the index moved lower.

SOLD 10 1/2 BACKRATIO SPX 100 (Weeklys) 26 AUG 22 3700/3500 PUT @ ~$0.13 Credit

SOLD 3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL @ ~$25.10 Credit

Sequence 2: While the S&P 500 was trading near $4,300.00 resistance, by 8/19/2022, all aforementioned Ratio Put Spread positions were rolled forward for a $452.26 credit.

The resulting position was as follows:

-17 1/2 BACKRATIO SPX 100 (Weeklys) 16 SEP 22 3700/3500 PUT

-3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL

From thereon the market declined and, by 9/1/2022, all positions were exited for a $6,963.84 credit.

BOT 17 1/2 BACKRATIO SPX 100 (Weeklys) 16 SEP 22 3700/3500 PUT @ ~$4.94 Credit

BOT 3 VERTICAL SPX 100 21 OCT 22 [AM] 4300/4350 CALL @ ~$4.57 Debit

Summary: In total, the sequence of trades net a $15,032.78 profit after commissions and fees.

The max loss (minus unforeseen events) sat at ~$6,790.00 if the market closed above $4,350.00 in OCT. Because the Ratio Put Spreads were initiated at no cost, any loss, if the market went higher, would have been the result of the trade’s Vertical Spread component. Overall, this trade netted in excess of a 200% return; the trade’s profit was more than two times the risk, a multi-bagger.

Reflection: Heading into the trade, it was the case that IVOL performed poorly during much of the 2022 decline. This was likely to remain the case on a subsequent drop, hence the wide and short-dated Ratio Put Spread.

Still, in spite of the Ratio Put Spread exposing the position to negative Delta and positive Gamma (i.e., the trade makes money if the market moves lower, all else equal), if implied skew became more convex (i.e., implied volatilities grow more rapidly as strike prices decrease), the position could have been a large loss.

So, if the flatter part of the skew curve (where the position was structured) became more convex, which is not something that was anticipated would happen, then the only recourse would have been to (1) close the position or (2) sell (i.e., add static negative Delta in) futures and correlated ETFs.

In the second case, then, the trade would have been allowed time to work and turn into a potential winner, particularly amidst the passage of time.

Additionally, in accordance with Physik Invest’s risk protocol, more units of the Short Put Ratio Spread could have been initiated on the transition into Sequence 2. These units could have been held through Labor Day, then, and monetized for up to an additional ~$4.00 credit per unit.

Though additional units of the Vertical Spreads could not have been added, due to the strict limits to debit risks, there were still months left to that particular component of the trade. With lower prices expected, there was little reason the Verticals should have been removed fast.

Going forward, should the context from a fundamental and volatility perspective remain the same, only on a rally could Physik Invest potentially re-enter a similar position.

Technical

As of 8:00 AM ET, Wednesday’s regular session (9:30 AM - 4:00 PM ET), in the S&P 500, is likely to open in the middle part of a balanced overnight inventory, inside of prior-range and -value, suggesting a limited potential for immediate directional opportunity.

In the best case, the S&P 500 trades higher.

Any activity above the $3,909.25 MCPOC puts into play the $3,952.75 LVNode. Initiative trade beyond the LVNode could reach as high as the $3,988.25 and $4,018.75 HVNode, or higher.

In the worst case, the S&P 500 trades lower.

Any activity below the $3,909.25 MCPOC puts into play the $3,884.25 LVNode. Initiative trade beyond the LVNode could reach as low as the $3,857.25 and $3,826.25 HVNode, or lower.

Click here to load today’s key levels into the web-based TradingView charting platform. Note that all levels are derived using the 65-minute timeframe. New links are produced, daily.

Considerations: Responsiveness near key-technical areas (that are discernable visually on a chart), suggests technically-driven traders with short time horizons are very active.

Such traders often lack the wherewithal to defend retests and, additionally, the type of trade may be indicative of the other time frame participants waiting for more information to initiate trades.

Definitions

Volume Areas: A structurally sound market will build on areas of high volume (HVNodes). Should the market trend for long periods of time, it will lack sound structure, identified as low volume areas (LVNodes). LVNodes denote directional conviction and ought to offer support on any test.

If participants were to auction and find acceptance into areas of prior low volume (LVNodes), then future discovery ought to be volatile and quick as participants look to HVNodes for favorable entry or exit.

MCPOCs: POCs are valuable as they denote areas where two-sided trade was most prevalent over numerous day sessions. Participants will respond to future tests of value as they offer favorable entry and exit.

About

After years of self-education, strategy development, mentorship, and trial-and-error, Renato Leonard Capelj began trading full-time and founded Physik Invest to detail his methods, research, and performance in the markets.

Capelj also develops insights around impactful options market dynamics at SpotGamma and is a Benzinga reporter.

Some of his works include conversations with ARK Invest’s Catherine Wood, investors Kevin O’Leary and John Chambers, FTX’s Sam Bankman-Fried, ex-Bridgewater Associate Andy Constan, Kai Volatility’s Cem Karsan, The Ambrus Group’s Kris Sidial, among many others.

Disclaimer

In no way should the materials herein be construed as advice. Derivatives carry a substantial risk of loss. All content is for informational purposes only.

Revisiting this now that I have more time to break it down. This is amazing! Makes me wish I could sit and walk through more of these ideas and concepts.

Fantastic job! Your Daily Brief is one of the few that I make certain to read as soon as it is available. Love your method of watching sentiment. Helps me get a “feel”, especially on days that I cannot dive in as early or as deeply as I want...

Really appreciated the more in-depth breakdown this time.

Have to ask: What program are you using to build this dashboard?